New report by NetBramha, powered by Poocho: How Indians decide whom to trust with their money →

Your savvy research assistant is here. Check out Poocho Studio.

How are Indian Millennials thinking about money in 2025? From saving for retirement to chasing financial independence, this generation is rewriting the rules of personal finance.

To explore this, we spoke in depth with 10 Millennials across India—from bustling metros to emerging Tier 2 hubs—to understand how they’re navigating money in 2025.

Their perspectives, shaped by different cities, incomes, and life stages, reveal a mix of tradition and innovation: mutual funds alongside stocks, neobanks alongside legacy banks, and advice from both finfluencers and family.

This report offers a close look at how this group of Millennials is saving, investing, and planning for the future.

Let's get into it.

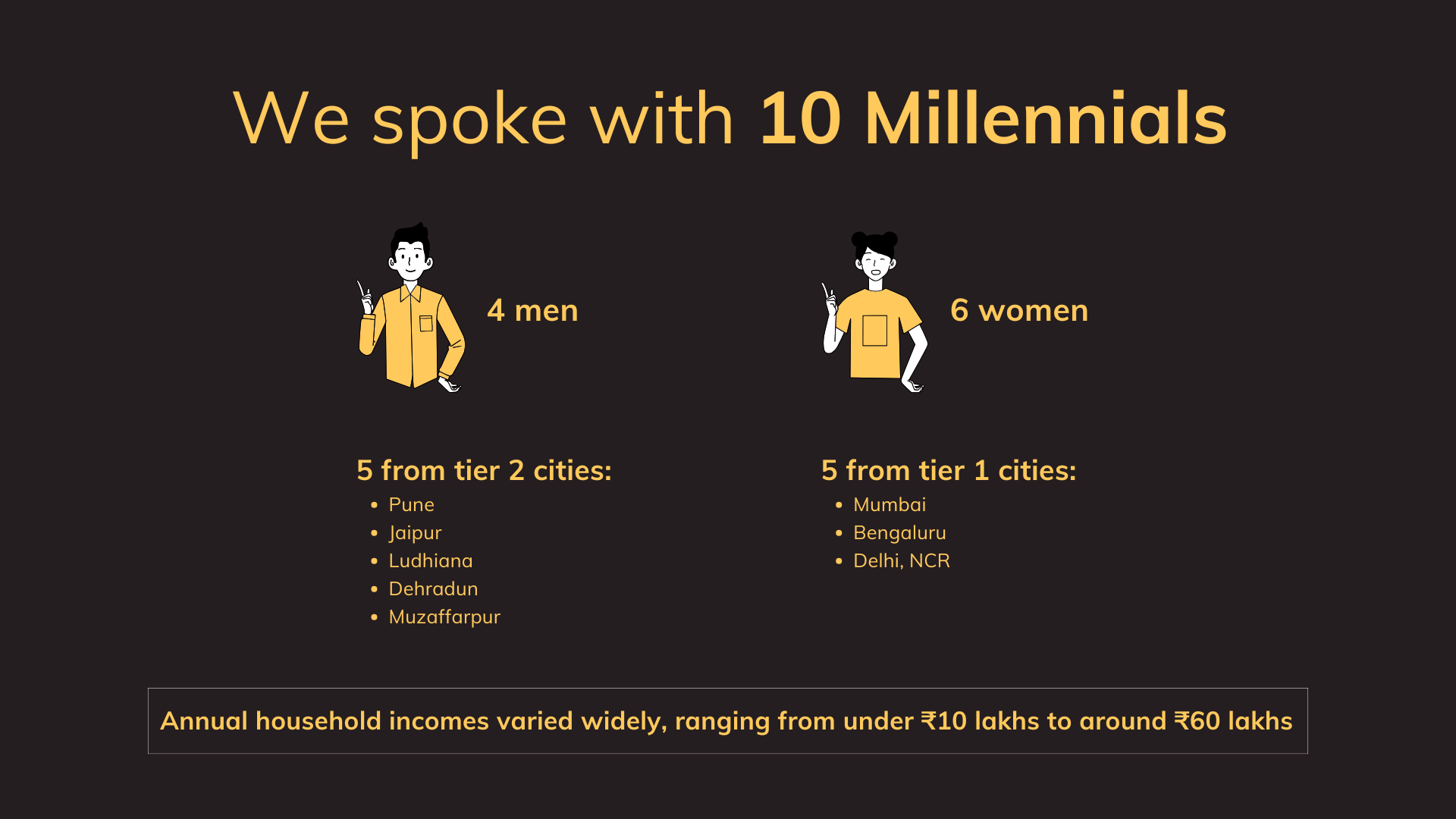

We spoke to 10 Millennials across India—4 men and 6 women— from tier 1 and tier 2 cities, with annual household incomes ranging from under ₹10 lakhs to around ₹60 lakhs.

In our interviews, participants mentioned a variety of apps they use for managing their investments, including Kuvera, INDmoney, and Zerodha. Among these, Groww emerged as the most frequently mentioned.

Participants praised Groww for its intuitive user interface, seamless user experience, and the convenience of tracking multiple assets and investment types—such as stocks and mutual funds—all in one platform.

Participants rely on a variety of resources to guide their investment decisions. Some delegate this responsibility to others, such as brokerage firms, relationship managers at trusted banks, or knowledgeable friends and family members.

Many also turn to online resources, including blogs, newspapers, and TV news channels, while a growing number follow "finfluencers" on social media for financial tips and insights. Among the most mentioned finfluencers were CA Rachna Ranade and Finance with Sharan.

For blogs and news apps, Moneycontrol stood out as the most frequently cited platform for staying updated on market trends and financial advice.

Participants mentioned both private and public sector banks in their responses. Among private sector banks, HDFC Bank was the most frequently cited, while SBI topped the list for public sector banks.

Notably, Millennials with accounts at SBI often shared that their parents initially chose the bank for them during childhood, and they have continued to maintain these accounts into adulthood.

Younger millennials also mentioned using neobanks such as Jupiter and FI Money.

When it comes to investment choices, Millennials in our study showed a strong preference for mutual funds and stocks, with each accounting for 21.9% of total mentions.

Fixed deposits remain a trusted option at 18.8% while gold (15.6%) and real estate (12.5%) continue to serve as long-term wealth preservation tools.

A smaller but notable share (9.4%) is allocated to other investments such as ESOPs and US stocks, indicating growing interest in diversified, global portfolios.

.png)

Among the mutual funds mentioned by participants, ICICI Prudential Fund received the highest number of mentions in our conversations.

Other mutual funds named included:

The chart below shows the count of mentions for each fund based on participant responses:

.png)

Millennials today are navigating money with both pragmatism and ambition. For some, the focus is on gaining financial independence and control over daily decisions, while for others, the dream is to retire early or become crorepatis by mid-life. Their approaches vary widely—shaped by gender, life stage, and personal aspirations

When it comes to saving, investing, and budgeting, millennial women present a diverse range of approaches shaped by their personal circumstances and experiences. Unless they have studied finance or work in the sector, many women rely on husbands, parents, or other male relatives for financial management and decision-making.

At the same time, some women are striving for greater financial independence. Participants like Minakshi and Gamini highlighted the importance of women taking control of their finances, emphasizing that independence in this area is key to personal and professional growth.

The evolving financial goals of women are also noteworthy. Himani, a 30-year-old participant, shared how her priorities have shifted over time. In her 20s, her focus was on traveling, owning a home, and shopping. Now, as a mother, much of her savings and investments are directed toward her son’s education, reflecting a significant change in her financial aspirations.

Many millennials dream of becoming crorepatis (millionaires) and retiring early, and they’re taking varied paths to achieve these ambitions. For some, this goal is tied to specific timelines—like Abhishek, who aims to reach this milestone by the age of 50-55. Tanisha, another participant, shares a similar aspiration.

Millennials are leveraging diverse strategies to build their wealth. Tanisha and Parth, both salaried employees, have invested in their companies’ stock options (ESOPs) as part of their financial growth plans. Others, like Paras, are exploring alternative avenues by saving to become silent partners in businesses, allowing them to earn profits without managing daily operations.

Abhishek, on the other hand, plans to launch a pharma business within the next 3-4 years as an additional income source. These varied approaches highlight millennials’ resourcefulness and determination to secure financial freedom on their own terms.

Through our research, some insights aligned with commonly held beliefs about Millennial financial habits.

These insights reinforce the idea that Millennial financial habits are shaped by a mix of generational, individual, and situational factors, with their choices reflecting a balance between their current needs and future goals.

This study was conducted end-to-end on the Poocho platform by Vaaruni Mahajan, UX Insights Manager at Poocho—from participant recruitment to interviews and analysis.

.png)

.png)