New report by NetBramha, powered by Poocho: How Indians decide whom to trust with their money →

Your savvy research assistant is here. Check out Poocho Studio.

Gen Z in India budgets in many ways. It’s less about the tool itself and more about creating a system they can tweak, expand, or abandon as their financial lives evolve.

SIPs anchor Gen Z's financial behaviour. Even risk-takers rely on SIPs as their long-term backbone, pairing them with stocks, crypto, or real estate based on comfort and life stage.

Gen Z in India wants growth, but need security and simplicity. They mix high-growth investments with safe options but wish for one consolidated app that brings it all together.

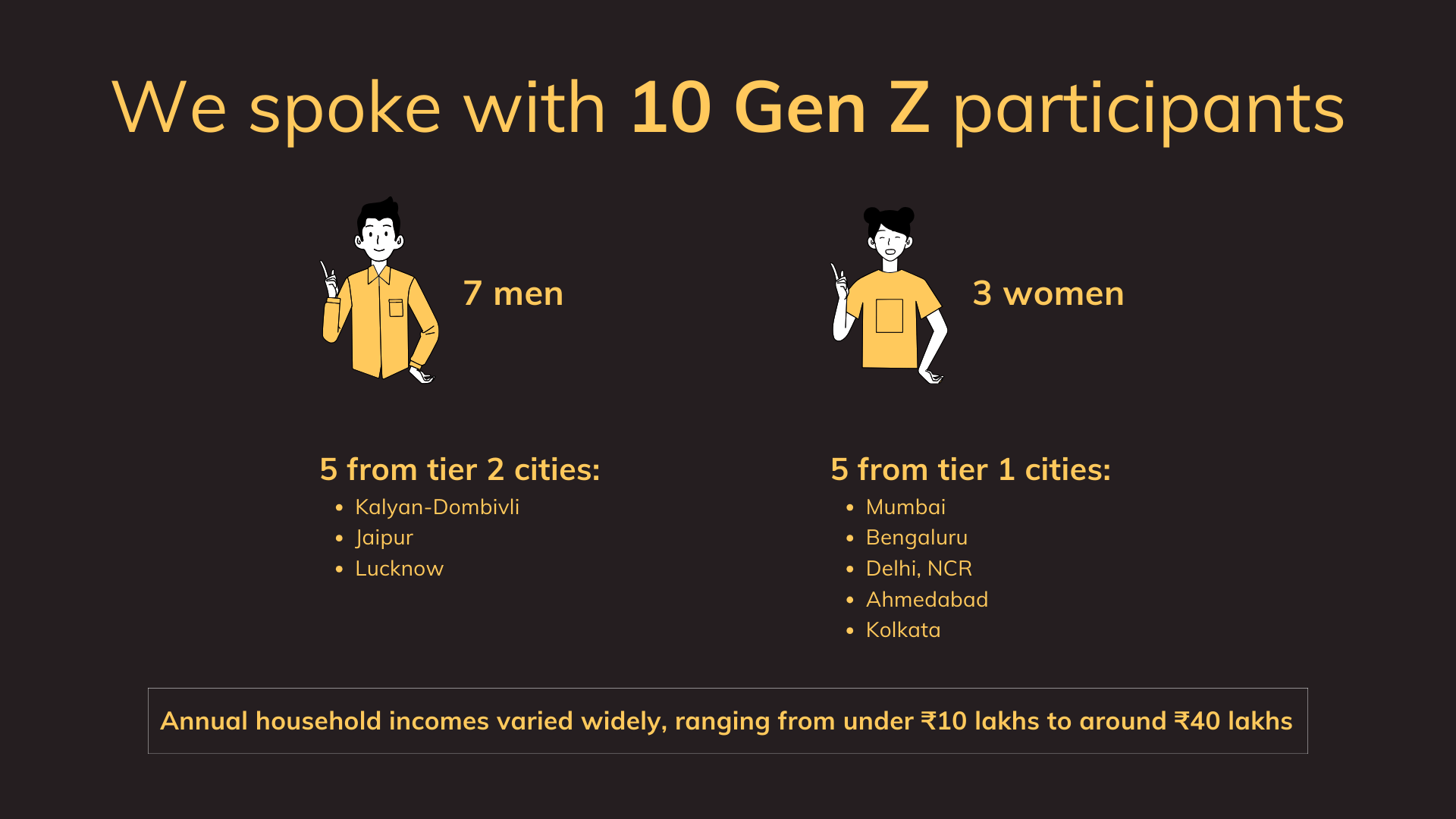

In continuation to our previous report on Millennials, we turned our attention to Gen Z (individuals aged 22 to 28 living across Tier-1 and Tier-2 Indian cities) to understand how they save, spend, and invest today. Unlike the Millennials who grew into financial independence gradually, this younger generation has entered adulthood amidst a boom of fintech apps, influencers, and easy access to market information.

Our conversations reveal a generation that’s curious, cautious, and deeply digital. While some experiment with high-risk assets like stocks or crypto, most combine them with steady SIPs and mutual funds to keep their finances balanced. The decision-making process is fast, informed, and often influenced by peers or content creators rather than traditional advisors such as family or money managers.

From using Groww, Zerodha, and INDmoney to track and invest, to following finance creators on Instagram or YouTube for quick learning, Gen Z’s financial playbook is built on accessibility and autonomy. Whether saving for a trip, a down payment, or just the comfort of having “something set aside,” their choices reflect both optimism and practicality.

This report dives into how they manage their money, what tools and products they trust, and how they’re shaping the next chapter of India’s financial story. Let's get into it.

We spoke to 10 Gen Z participants across India—7 men and 3 women—from tier 1 and tier 2 cities.

Annual household income:

– INR 10–30 lakhs (9 participants)

– INR 30–60 lakhs (1 participant)

Living situations: A mix of living with parents, shared accommodation/roommates, hostels, and family homes.

Employment status: Students (medical and engineering), early-career professionals across consulting, healthcare, logistics, EdTech, and software, along with one entrepreneur-in-residence and a few participants running side hustles.

Money behaviours shifted noticeably by life stage. Students tended to prefer safer instruments like Systematic Investment Plans (SIPs) and Fixed Deposits, keeping their focus on stability while managing limited income. Those who had just entered the workforce were more experimental, some stayed loyal to SIPs, while others ventured into direct stocks or crypto to explore higher returns. A few participants with strong family financial backing, such as entrepreneurs or salaried individuals from business families, had already diversified into real estate, treating it as a long-term and reliable asset. Together, these choices reflect how financial comfort and confidence evolve with age, income, and exposure.

When it comes to investing, Gen Z isn’t short on options but a few platforms clearly dominate.

Groww emerged as the go-to app for most participants. Its simple UI, fast onboarding, and seamless SIP setup make it feel almost effortless to start investing. For many, Groww was their “first step” into the world of mutual funds and direct stocks — an app that makes investing feel less intimidating.

Other frequently mentioned platforms included Zerodha (Kite & Coin) for direct equity and smooth transfers, INDmoney for portfolio tracking and mutual fund discovery, and Upstox or Angel One for those more inclined toward active trading. A few participants also mentioned Binance for crypto holdings, ET Money and Cred for tracking and credit management, and neobanks like Jupiter and Fi Money for everyday money management. One participant even used KoShaX to invest in digital gold.

What makes these tools stick?

Social media is often the spark. Instagram pages, finance reels, and influencer accounts like One Vision 99 Media are where financial curiosity begins. Quick, catchy videos introduce young people to new apps, products, or ideas and make investing feel approachable rather than intimidating.

Once something catches their eye, they turn to trusted sources like LiveMint, Moneycontrol, The Economic Times, or even a quick Google News search to dig deeper. For some, finance newsletters and curated feeds help them stay informed without endless scrolling.

Despite being digital natives, family and peers still play a big role. Parents, siblings, and friends offer the validation they need to make decisions. Family habits often shape early investment behaviour, while peer recommendations influence app choices and comfort with risk.

Even apps are teachers now. Platforms like Groww, INDmoney, and Zerodha have built-in explainers, articles, and nudges that help users learn as they invest. Many said they picked up the basics directly from the tools they use every day.

It’s a blended information diet; social-first for discovery, trusted media for depth, and family or peers for reassurance. This generation isn’t waiting for formal education to catch up; they’re building financial literacy in real time, one reel or app notification at a time.

Budgeting takes many forms. Some prefer the structure of Notion templates, while others rely on Excel spreadsheets for monthly tracking. It’s less about the tool itself and more about creating a system they can tweak, expand, or abandon as their financial lives evolve.

Credit cards are treated like strategy games. Many take full advantage of reward programs and use apps like CRED to manage payments, track due dates, and maximise cashback or points. It’s both a practical and satisfying way to make spending feel a little smarter.

For some, security means liquidity. One participant keeps ₹5–6 lakh in cash savings simply for “mental comfort,” describing it as a buffer that makes them feel at ease, even if it’s not the most efficient use of money.

Neo-banks have also carved out a space in their routines. They’re valued for convenience, modern interfaces, and features traditional banks often lack such as instant notifications to smoother app experiences.

A recurring frustration, however, lies in the fragmentation of their financial world. Many juggle multiple apps to track investments, budgets, and savings, and wish for one consolidated view that brings it all together.

To understand how Gen Z is approaching investing, we asked participants where they currently park their money across different asset classes. Their responses reveal a clear preference for market-linked instruments, alongside continued trust in traditional, lower-risk options.

While equities and mutual funds dominate Gen Z portfolios, fixed deposits and gold still play a meaningful role. A smaller share of investments flows into alternative assets such as real estate, crypto, and corporate bonds.

For many young adults, the first taste of financial independence came with a wave of impulsive spending and the lessons that followed.

Rahul, 24, recalls how managing his own money abroad led to a period of unchecked spending until a medical emergency forced him to become disciplined.

"I was very much of an impulsive person as well. When I went to China and I was supposed to manage my own expenses, the first two months I faltered very much. Like I was like, okay, itna paisa hai, uda do uda do [I have so much money, spend it, spend it]...I got frostbite. And I had medical expenses to incur. And I was like, okay, I did not save up for this. . . So I had to ask my friends for money and stuff. That is very something that I would never want to do again. So that is why the rigidity came in.”

- Rahul, 24

Mitali, 27, shared a similar journey of overconsumption after landing her first job. She described how, as a woman, constant consumerism — from skincare to clothing — made restraint difficult until she consciously shifted toward buying only what she needed and prioritising experiences instead.

"When I got my first job, I started spending a lot — all the shopping apps unlocked at once. As a woman, there’s so much consumerism pushed at you — skincare, clothes, makeup. Eventually, I realised how pointless it was. Now I only buy things when I run out and prefer spending on experiences instead.”

- Mitali, 27

Across stories like these, the pattern is clear: financial maturity often begins with mistakes. Over time, impulsive spending gives way to intentional, value-driven choices.

While Gen Z’s financial habits are shaped by apps, social media, and flexible income streams, their long-term aspirations often echo the generations before them. Owning a home and a car continues to hold symbolic power. Not just as financial goals, but as markers of stability, independence, and success.

For Mahesh, 27, the next couple of years are all about building or buying a home. It symbolises a tangible step toward security. Sahil, 27, frames it more broadly: these are “basic goals” most people grow up with, ingrained early as signs of having “made it.” And for Arjun, 25, the dream is more personal and aspirational. He knows exactly what he wants: a Range Rover.

“So as of now, I will say, a home would be the most important thing for me in the upcoming year or two. So buying a home or building a new home is a goal”

- Mahesh, 27

“I think two basic goals every, every I think the two basic goals everyone has - I don't want to generalize it, but something that we sort of engrain while growing up is having your own car and a house"

- Sahil, 27

"I definitely am going to buy a Range Rover"

- Arjun, 25

Across conversations, these ambitions reveal how deeply emotional financial planning can be. Even among a generation known for valuing flexibility and experiences over possessions, there’s still a strong pull toward permanence and wanting something to show for their hard work. For some, it’s a practical next step; for others, it’s about identity and pride. But for nearly everyone, these goals signal one thing clearly: financial independence is as much about emotional fulfillment as it is about numbers on a balance sheet.

Short answer: both.

Validated:

Invalidated or nuanced:

Some other insights and patterns observed include:

This cohort approaches money with equal parts curiosity and control. They’re eager to grow their wealth but aren’t reckless about it. Most rely on SIPs as their steady, disciplined foundation. It’s viewed as a simple way to invest regularly without overthinking. Alongside that, fixed deposits, emergency funds, and large cash buffers act as safety nets that help them feel secure.

Many dabble in direct stocks and crypto for higher returns or out of genuine interest, while others see real estate as a more grounded, long-term play. Their financial curiosity is fed by a mix of modern and traditional sources; a reel might spark the idea, but they’ll fact-check it before acting.

In short, they’re not chasing quick wins. They’re experimenting, learning, and building financial confidence one investment at a time.

This study was conducted end-to-end on the Poocho platform by Vaaruni Mahajan, UX Insights Manager at Poocho—from participant recruitment to interviews and analysis.

*participant names have been changed to protect their privacy

.png)

.png)